Understanding Michael Porter

Porter took a different path, creating what he calls “frameworks.” In his own words:

“My frameworks provide a set of logical relationships that are really fundamental. They’re like physics—if you’re going to have higher profitability, you’ve got to have a higher price or a lower cost. That industry competition is driven by the five forces. That the firm is a collection of activities. These frameworks provide basic, fundamental, and I believe unchangeable relationships about the ‘matter’ of competition.”

The key to competitive success—for businesses and nonprofits alike—lies in an organization’s ability to create unique value. Porter’s prescription: aim to be unique, not best. Creating value, not beating rivals, is at the heart of competition.

Strategy explains how an organization, faced with competition, will achieve superior performance.

How you think about competition will define the choices you make about how you are going to compete. It will impact your ability to assess those choices critically. That is why before we can even begin to talk about strategy, we need to tackle the question of competition and competitive advantage.

The airline industry has suffered from this sort of competition for decades. If American Airlines tries to win new customers by offering free meals on its New York to Miami route, then Delta will be forced to match it—leaving both companies worse off. Both will have incurred added costs, but neither will be able to charge more, and neither will end up with more seats filled. Every time one company makes a move, its rivals will jump to match it. With everyone chasing after the same customer, there will be a contest over every sale. This, says Porter, is competitive convergence. Over time, rivals begin to look alike as one difference after another erodes. Customers are left with nothing but price as the basis for their choices. This has happened in airlines, in many categories of consumer electronics, and in personal computers, with the notable exception of Apple, the one major company in that industry that has consistently marched to its own drummer.

As you might expect, rivals didn’t take long to respond, piling on the pillows and swaddling guests in ever-higher thread counts: Hilton with its Serenity Bed, Marriott with its Revive Collection, Hyatt with its Hyatt Grant Bed, Radisson with its Sleep Number Bed, and Crowne Plaza with its Sleep Advantage Program. By 2006, the press declared that the Bed Wars had come to an end, but not before every major rival had made large investments developing, installing, and promoting its own branded offering. Guests at every hotel in the category can now rest assured that “bed quality” will not differentiate one hotel from another. As is often the case, one company’s attempt to be “the best” ended up raising the bar for everyone. It’s not surprising, with this approach to competing, that long-term profitability in the hotel industry has been chronically low, a topic we’ll explore more rigorously in chapter 2. Reports are mixed about whether, in this case, the industry was able to raise prices enough to benefit from its investment in upgraded bedding. If not, customers captured the value of this spending. But even if this particular move benefited the industry overall, when all rivals compete on the same dimension, no one gains a competitive advantage.

Companies only have to be “big enough,” which rarely means they have to dominate. Often “big enough” is just 10 percent of the market. Yet companies under the influence of winner-takes-all thinking tend to pursue illusory scale advantages. In doing so, they are likely to damage their own performance by cutting price to gain volume, by overextending themselves to serve all market segments, and by pursuing overpriced mergers and acquisitions. The auto industry over the past couple of decades has exhibited all of the above tendencies, to disastrous effect.

Competing to be unique is unlike warfare in that one company’s success does not require its rivals to fail. It is unlike competition in sports because every company can chose to invent its own game. A better analogy than war or sports might be the performing arts. There can be many good singers or actors—each outstanding and successful in a distinctive way. Each finds and creates an audience. The more good performers there are, the more audiences grow and the arts flourish. This kind of value creation is the essence of positive-sum competition.

While zero-sum competition is rightly depicted as a race to the bottom, positive-sum competition produces better outcomes. To be sure, not every company will succeed. Competition will weed out the underperformers. But companies that do a good job can earn sustainable returns because they create more value; nonprofit organizations can do more good because they meet needs more effectively and efficiently. And customers can get real choice in how their needs are met. Competing to be the best feeds on imitation. Competing to be unique thrives on innovation.

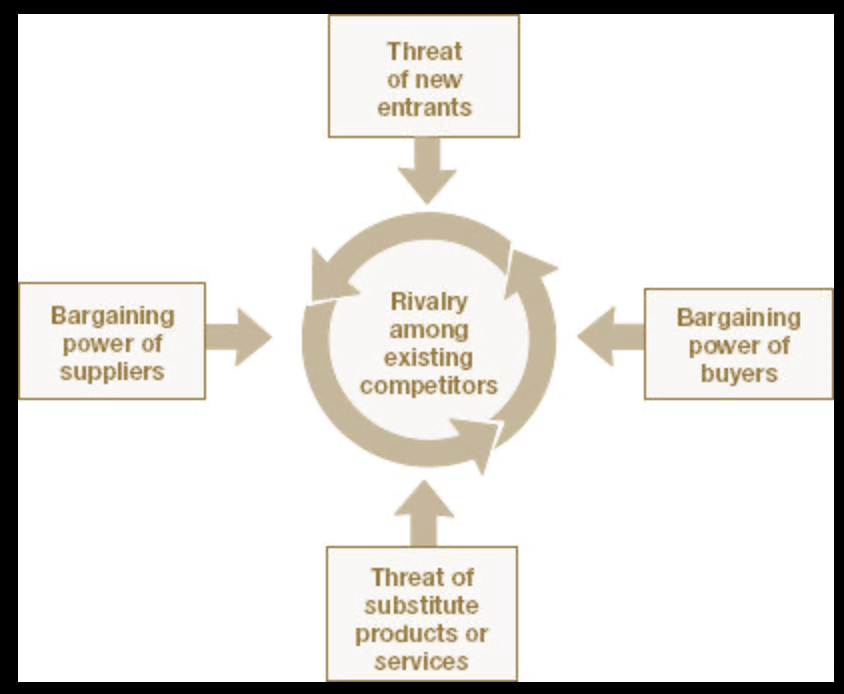

FIGURE 2-1 Industry structure: The five forces

Porter’s research findings on the links between industry structure and profitability challenge several popular misconceptions. Porter has, in fact, found: First, as different from one another as industries might appear on the surface, the same forces are at work under the skin. From advertising to zipper manufacturing (and every industry in between), the same five forces apply, although their relative strength and importance may differ. Second, industry structure determines profitability—not, as many people think, whether the industry is high growth or low, high tech or low, regulated or not, manufacturing or service. Structure trumps these other, more intuitive, categories. Third, industry structure is surprisingly sticky. Despite the prevailing sense that business changes with incredible rapidity, Porter discovered that industry structure—once an industry passes beyond its emerging, prestructure phase—tends to be quite stable over time. New products come and go. New technologies come and go. Things change all the time. But structural change—and therefore change in the average profitability of an industry—usually takes a long time.

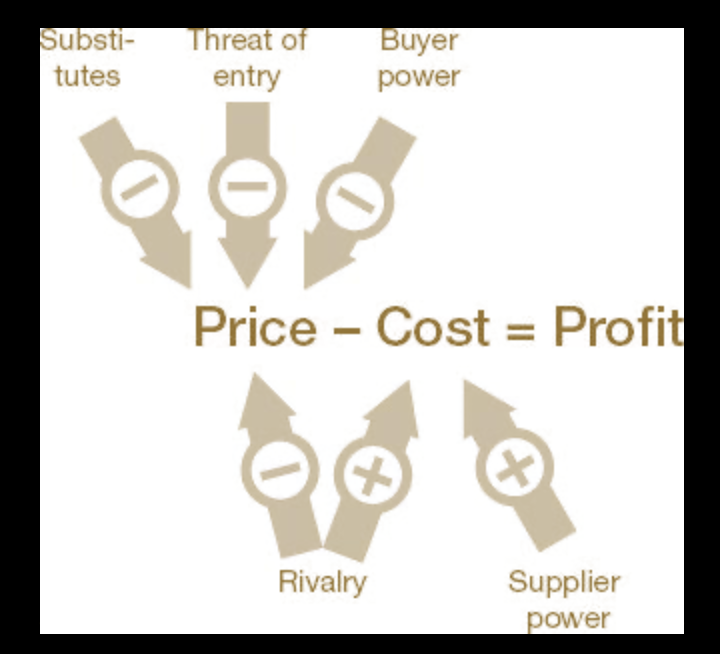

The five forces framework explains the industry’s average prices and costs, and therefore the average industry profitability you are trying to beat.

Each of the five forces has a clear, direct, and predictable relationship to industry profitability. Here’s the general rule: the more powerful the force, the more pressure it will put on prices or costs or both, and therefore the less attractive the industry will be to its incumbents. (A reminder: Industry structure is always analyzed from the perspective of companies already in the industry. Because potential entrants must overcome entry barriers, this explains why an industry can be “attractive” to incumbents while at the same time not attracting new competitors.)

Powerful buyers will force prices down or demand more value in the product, thus capturing more of the value for themselves.

Substitutes—products or services that meet the same basic need as the industry’s product in a different way—put a cap on industry profitability

Entry barriers protect an industry from newcomers who would add new capacity.

If rivalry is intense, companies compete away the value they create, passing it on to buyers in lower prices or dissipating it in higher costs of competing.

The five forces framework applies in all industries for the simple reason that it encompasses relationships fundamental to all commerce.

there are a limited number of structural forces at work in every industry that systematically impact profitability in a predictable direction.

Other factors may be important, but they are not structural. Consider four that get the most attention:

- Government regulation will be relevant to competition if it changes the industry’s structure through its impact on one or more of the five forces.

- The same goes for technology. If the Internet, for example, makes it easier for customers in an industry to shop around for the best price, then industry profitability will drop because, in this instance, the Internet has changed the industry’s structure by increasing the power of buyers.

- Managers often mistakenly assume that a high-growth industry will be an attractive one. But growth is no guarantee that the industry will be profitable. For example, growth might put suppliers in the driver’s seat, or, combined with low entry barriers, growth might attract new rivals. Growth alone says nothing about the power of customers or the availability of substitutes. The untested assumption that a fast-growing industry is a “good” industry, Porter warns, often leads to bad strategy decisions.

- Finally, complements are sometimes proposed as a “sixth force.” Complements are products and services used together with an industry’s products—for example, computer hardware and software.

How the 5 forces affect profitability

Industry structure determines how the economic value created by an industry is divided—how much is captured by companies in the industry versus customers, suppliers, distributors, substitutes, and potential new entrants. Industry structure can be linked directly to the income statements and balance sheets of every company in the industry. The insights gained from this kind of analysis should lead directly to decisions about where and how to compete.

How can you use industry analysis? Consider two representative examples. First, does the industry offer the possibility of attractive returns? In 2005, IBM sold its PC business to Lenovo. A five forces analysis makes clear immediately why the business had become so unattractive that even one of its marquee players decided to throw in the towel. Its two superpower suppliers, Microsoft and Intel, captured almost all of the value the industry created. And as the industry matured, the PC itself had become a commodity, giving customers more power. Since one beige box was as good as another, customers could easily switch brands in order to get a good price. Rivalry among PC makers was intensifying, with more price pressure coming from emerging Asian producers. To top it off, a new generation of potential substitutes was taking off—a range of mobile devices that had some of the same functionality as PCs.

Typical Steps in Industry Analysis

- Define the relevant industry by both its product scope and geographic scope. What’s in, what’s out? This step is trickier than most people realize, so give it some real thought. The five forces help you draw the boundaries, avoiding the common pitfall of defining the industry too narrowly or too broadly. Are you facing the same buyers, the same suppliers, the same entry barriers, and so forth? Porter offers this rule of thumb: where there are differences in more than one force, or where differences in any one force are large, you are likely dealing with distinct industries. Each will need its own strategy. Consider these examples:

- Product scope. Is motor oil used in cars part of the same industry as motor oil used in trucks and stationary engines? The oil itself is similar. But automotive oil is marketed through consumer advertising, sold to fragmented customers through powerful channels, and produced locally to offset the high logistics costs of small packaging. Truck and power generation lubricants face a different industry structure—different customers and selling channels, different supply chains, and so on. From a strategy perspective, these are distinct industries.

- Geographic scope. Is the cement business global or national? Recall the CEMEX example discussed earlier. Although some elements are the same, buyers are radically different in the United States and Mexico. The geographic scope is national, not global, and CEMEX will need a separate strategy for each market.

- Identify the players constituting each of the five forces and, where appropriate, segment them into groups. On what basis do these segments emerge?

- Assess the underlying drivers of each force. Which are strong? Which are weak? Why? The more rigorous your analysis, the more valuable your results.

- Step back and assess the overall industry structure. Which forces control profitability? Not all are equally important. Dig deeper into the most important forces in your industry. Are your results consistent with the industry’s level of profitability today and over the long term? Are the more profitable companies better positioned in relation to the five forces?

- Analyze recent and likely future changes for each force. How are they trending? Looking ahead, how might competitors or new entrants influence industry structure?

- How can you position yourself in relation to the five forces? Can you find a position where the forces are weakest? Can you exploit industry change? Can you reshape structure in your favor?

Can you position your company where the forces are weakest? Consider the strategy developed by heavy-truck maker Paccar. This is another industry with an uninviting structure: There are many big, powerful buyers who operate large fleets of trucks; they are price sensitive because trucks represent a large piece of their costs. Rivalry is based on price because (a) the industry is capital intensive, with cyclical downturns, and (b) most trucks are built to regulated standards and therefore look the same. On the supplier side, unions exercise considerable power, as do the large independent suppliers of engines and drive train components. Truck buyers face substitutes for their services (rail, for example), which puts an overall cap on truck prices.

Between 1993 and 2007, the industry average return on invested capital (ROIC) was 10.5 percent. Yet over the same period Paccar, a company with about 20 percent of the North American heavy-truck market, earned 31.6 percent. Paccar has developed a positioning within this difficult industry where the forces are the weakest. Its target customer is the individual owner-operator, the guy whose truck is his home away from home. This customer will pay more for the status conferred by Paccar’s Kenworth and Peterbilt brands and for the ability to add a slew of custom features such as a luxurious sleeper cabin or plush leather seats. Paccar’s made-to-order products come with a number of accompanying services geared to make the owner-operator more successful. For example, Paccar’s roadside assistance program limits downtime, a key to the owner’s economics. In an industry marked by price competition, Paccar is able to charge a 10 percent price premium. Paccar doesn’t try to compete by being the “best” truck maker in the industry. If it did, it would go after the same customers with the same products. It would get caught up in the industry’s price competition, intensifying rivalry, which would erode its advantage.

If you have a competitive advantage, then, your profitability will be sustainably higher than the industry average (see figure 3-1). You will be able to command a higher relative price or to operate at a lower relative cost, or both. Conversely, if a company is less profitable than its rivals, by definition it has lower relative prices or higher relative costs, or both. This basic economic relationship between relative price and relative cost is the starting point for understanding how companies create competitive advantage.

From here Porter takes us through a thought process that’s a lot like peeling an onion. First, disaggregate the overall profitability number into its two components, price and cost. This is done because the underlying causal factors, the drivers of price and cost, are so different, and the implications for action are different as well.

Relative Price A company can sustain a premium price only if it offers something that is both unique and valuable to its customers. Apple’s hot, must-have gadgets have commanded premium prices. Ditto for the high-speed Madrid-to-Barcelona train and the trucks Paccar creates for owner-operators. Create more buyer value and you raise what economists call willingness to pay (WTP), the mechanism that makes it possible for a company to charge a higher price relative to rival offerings.

Product scope. Is motor oil used in cars part of the same industry as motor oil used in trucks and stationary engines? The oil itself is similar. But automotive oil is marketed through consumer advertising, sold to fragmented customers through powerful channels, and produced locally to offset the high logistics costs of small packaging. Truck and power generation lubricants face a different industry structure—different customers and selling channels, different supply chains, and so on. From a strategy perspective, these are distinct industries. Geographic scope. Is the cement business global or national? Recall the CEMEX example discussed earlier. Although some elements are the same, buyers are radically different in the United States and Mexico. The geographic scope is national, not global, and CEMEX will need a separate strategy for each market.

If you have a real competitive advantage, it means that compared with rivals, you operate at a lower cost, command a premium price, or both.

Dell Inc.’s low relative costs up through the early 2000s came from both sources. Vertically integrated rivals, such as Hewlett-Packard, designed and manufactured their own components, built computers to inventory, and then sold them through resellers. Dell sold direct, building computers to customer orders using outsourced components and a tightly managed supply chain. These competing approaches had very different cost and investment profiles. Dell’s model required little capital since the company did not design or make components, nor did it carry much inventory. In the late 1990s, Dell had a substantial advantage in days of inventory carried. Because component costs were then dropping so fast, buying components weeks later, as Dell effectively did, translated into lower relative costs per PC. And Dell’s customers actually paid for their PCs before Dell had to pay its suppliers. Most companies have to finance the working capital they need to run their business. Dell’s strategy resulted in negative working capital, which further enhanced Dell’s cost advantage.

The second component of superior profitability is relative cost—that is, you manage somehow to produce at lower cost than your rivals. To do so, you have to find more efficient ways to create, produce, deliver, sell, and support your product or service. Your cost advantage might come from lower operating costs or from using capital more efficiently (including working capital), or both.

Start by laying out the industry value chain. Every established industry has one or more dominant approaches. These reflect the scope and sequence of activities that most of the companies in that industry perform, and this is as true for nonprofits as for any business. The industry’s value chain is effectively its prevailing business model, the way it creates value (see figure 3-2). It is where most companies in the industry have chosen “to sit” in relation to the larger value system. FIGURE 3-2 The value chain: Configuring activities to create customer value How far upstream or downstream do the industry’s activities extend? What are the key value-creating activities at each step in the chain? Compare the value chains of rivals in an industry to understand differences in prices and costs

Strategy choices aim to shift relative price or relative cost in a company’s favor.

The sequence of activities your company performs to design, produce, sell, deliver, and support its products is called the value chain. In turn, your value chain is part of a larger value system

We now have a concise, concrete definition of competitive advantage: superior performance resulting from sustainably higher prices, lower costs, or both. But we have to peel one final layer of the onion to arrive at what I’ll call the managerially relevant sources of competitive advantage—the things that managers can control. Ultimately, all cost or price differences between rivals arise from the hundreds of activities that companies perform as they compete.

Zero in on price drivers, those activities that have a high current or potential impact on differentiation. Do you or could you create superior value for your customers by performing activities in a distinctive way or by performing activities that competitors don’t perform? Can you create that value without incurring commensurate costs? Buyer value can arise throughout the value chain. It can come from product design, for example, as it does for Whirlwind Wheelchair. It can come from choices in the inputs used or the production process itself, both of which are key to the success of In-N-Out Burger, a chain of over 230 hamburger restaurants that uses only the freshest ingredients and prepares its limited menu on-site

- Zero in on cost drivers, paying special attention to activities that represent a large or growing percentage of costs.

Your relative cost position (RCP) is built up from the cumulative cost of performing all the activities in the value chain. Are there actual or potential differences between your cost structure and those of your rivals? The challenge here is to get as accurate a picture as you can of the full costs associated with each activity, including not only direct operating and asset costs but also the overhead costs that are generated because you perform this activity

Competitive advantage arises from the activities in a company’s value chain

We now have a complete definition of competitive advantage: a difference in relative price or relative costs that arises because of differences in the activities being performed

Wherever a company has achieved competitive advantage, there must be differences in activities. But those differences can take two distinct forms. A company can be better at performing the same configuration of activities, or it can choose a different configuration of activities. By now, of course, you recognize that the first approach is competition to be the best. And by now, we are in a better position to understand why this approach is unlikely to produce a competitive advantage.

Porter uses the phrase operational effectiveness (OE) to refer to a company’s ability to perform similar activities better than rivals. Most managers use the term “best practice” or “execution.” Whichever term you prefer, we are talking about a multitude of practices that allow a company to get more out of the resources it uses. The important thing is not to confuse OE with strategy.

No company can afford sloppy execution. Inefficiency can overwhelm even the most distinctive and potentially valuable strategies. But betting that you can achieve competitive advantage—a sustainable difference in price or cost—by performing the same activities as your rivals is a bet you will probably lose. No one has been better at OE competition than the Japanese, but, as Porter’s work documents in great detail, OE competition has led even the best of them to chronically poor profitability

Popular metrics such as shareholder value, return on sales, growth, and market share are misleading for strategy. The goal of strategy is to earn superior returns on the resources you deploy, and that is best measured by return on invested capital. Competitive advantage is not about beating rivals; it’s about creating superior value and about driving a wider wedge than rivals between buyer value and cost. Competitive advantage means you will be able to sustain higher relative prices or lower relative costs, or both, than your rivals in an industry. If you have a competitive advantage, it will show up on your P&L.

Differences in relative prices and relative costs can ultimately be traced to the activities that companies perform. A company’s value chain is the collection of all its value-creating and cost-generating activities. The activities, and the overall value chain in which activities are embedded, are the basic units of competitive advantage.

The value proposition is the element of strategy that looks outward at customers, at the demand side of the business. The value chain focuses internally on operations. Strategy is fundamentally integrative, bringing the demand and supply sides together.

Good strategies depend on many choices, not one, and on the connections among them. A core competence alone will rarely produce a sustainable competitive advantage. Flexibility in the face of uncertainty may sound like a good idea, but it means that your organization will never stand for anything or become good at anything. Too much change can be just as disastrous for strategy as too little. Committing to a strategy does not require heroic predictions about the future. Making that commitment actually improves your ability to innovate and to adapt to turbulence.

The activities companies perform are the basic units of competitive advantage because they are the ultimate source of both relative costs and the levels of differentiation a company can offer its customers.

Vying to be the best is an intuitive but self-destructive approach to competition. There is no honor in size or growth if those are profitless. Competition is about profits, not market share. Competitive advantage is not about beating rivals; it’s about creating unique value for customers. If you have a competitive advantage, it will show up on your P&L. A distinctive value proposition is essential for strategy. But strategy is more than marketing. If your value proposition doesn’t require a specifically tailored value chain to deliver it, it will have no strategic relevance. Don’t feel you have to “delight” every possible customer out there. The sign of a good strategy is that it deliberately makes some customers unhappy. No strategy is meaningful unless it makes clear what the organization will not do. Making trade-offs is the linchpin that makes competitive advantage possible and sustainable. Don’t overestimate or underestimate the importance of good execution. It’s unlikely to be a source of a sustainable advantage, but without it even the most brilliant strategy will fail to produce superior performance.

You need only a very broad sense of which customers and needs are going to be relatively robust five or ten years from now. Strategy is implicitly a bet that the chosen customers or needs—and the essential trade-offs for meeting them at the right price—will be enduring.

That’s where stability is most important—in the basic value proposition, the core of needs the company meets and its relative price.

Despite five decades of dramatic change in the merchandise it sells, modifications in its store formats and systems, and continuous improvements in productivity, the basic value proposition is unchanged: Walmart continues to offer its customers branded merchandise at everyday low prices.

Aravind Eye Care makes cataract surgery affordable. From its very humble origins in 1976, starting with three doctors and eleven beds, there have been vast changes in both Aravind’s scale and scope, but it continues to serve the enduring need for affordable eye care.

Continuity of strategy does not mean that an organization should stand still. As long as there is stability in the core value proposition, there can, and should, be enormous innovation in how it’s delivered

Continuity fosters improvements in individual activities and fit across activities; it allows an organization to build unique capabilities and skills tailored to its strategy

Continuity has enabled the Swiss food giant Nestlé to develop a thriving supply base of local farmers for its milk business in India. Starting in the 1960s with just 180 farmers, Nestlé built refrigerated dairies as collection points for milk. Over time it provided technical assistance, training, and supplies to the farmers, who have become vastly more productive (and prosperous) as a result. The number of farmers working with Nestlé has grown to over 75,000.

Continuity helps suppliers, channels, and other outside parties to contribute to a company’s competitive advantage

Continuity reinforces a company’s identity—it builds a company’s brand, its reputation, and its customer relationships

Continuity reinforces a company’s identity—it builds a company’s brand, its reputation, and its customer relationships.

The standard argument has been that companies should focus on their core activities. Those that aren’t “core” can be outsourced to more efficient providers. But once you appreciate the role of fit, you will stop and think much harder about outsourcing. Instead of trying to determine which activities are core, Porter asks a different question: Which activities are generic and which are tailored? Generic activities—those that cannot be meaningfully tailored to a company’s position—can be safely outsourced to more efficient external suppliers. However, Porter argues that outsourcing is risky for activities that are or could be tailored to strategy, and especially for those activities that are strongly complementary with others. The fewer elements that remain in the company’s value chain, the fewer the opportunities to extend tailoring, trade-offs, and fit.

A common mistake in strategy is to choose the same core competences as everyone else in your industry.

Fit means that the value or cost of one activity is affected by the way other activities are performed.

Flat packs, as we saw in chapter 5, play a big role in IKEA’s competitive advantage because they lower the costs of shipping and product damage. So as an independent choice, flat packs support IKEA’s low-price positioning. Suburban store locations lower costs because land is cheaper outside the city limits. But these two choices are, of course, interdependent. The value of those flat packs is amplified by the car-friendly locations that make it easier for customers to load their purchases into their cars. Go down the list of activities and you will see many such examples of fit. Huge stores amplify the value of global-scale product sourcing. Huge stores are more valuable if customers are willing to spend more time per visit. The free childcare and the in-house cafeteria make it possible (and even enjoyable, if you like Swedish meatballs) for customers to take their time. Each of these choices enhances the value of the others. All contribute to lower prices for customers. The huge store format gives IKEA space to showcase all its merchandise in fully decorated room displays. These, along with the large product information hang-tags, allow IKEA to do without sales representatives.

Good strategies depend on the connection among many things, on making interdependent choices.

Fit has to do with how the activities in the value chain relate to one another. Its role in strategy highlights yet another popular misconception, that competitive success can be explained by one core competence, the one thing you do really well. The fallacy here is that good strategies don’t rely on just one thing, on making one choice. Nor do they typically result from even a series of independent choices. Good strategies depend on the connection among many things, on making interdependent choices.

Trade-offs like these are never easy. Make no mistake, Edward Jones has left money on the table. But at the same time, it has mastered what Porter calls one of the great paradoxes about trade-offs in competition. Executives often resist making trade-offs for fear they will lose some customers. The irony is that unless they make trade-offs and deliberately choose not to serve all customers and needs, then they are unlikely to do a good job of serving any customers and needs.

Trade-offs are the strategic equivalent of a fork in the road. If you take one path, you cannot simultaneously take the other.

Thus the value proposition and the value chain—the two core dimensions of strategic choice—are inextricably linked. The value proposition focuses externally on the customer. The value chain focuses internally on operations. Strategy is fundamentally integrative, bringing the demand and supply sides together.

This is a crucially important test that should be applied to any strategy. If the same value chain can deliver different value propositions equally well, then those value propositions have no strategic relevance. Only a value proposition that requires a tailored value chain to deliver it can serve as the basis for a robust strategy. This is the first line of defense against rivals.

Choices in the value proposition that limit what a company will do are essential to strategy because they create the opportunity to tailor activities in a way that best delivers that kind of value.

Tailoring is possible only if there are limits, only if you are not trying to be all things to all people. In other words, limits make it possible to develop a value chain that is different from rivals.

The results speak for themselves: Aravind, in 2009–2010, performed about 5 percent of all eye surgeries in India, employing only 1 percent of the nation’s ophthalmic manpower. The achievement mirrors that of Henry Ford’s assembly line for the Model T, which made Ford workers five times more productive than the auto industry average. Aravind has made cataract surgery affordable by applying the core design elements that Ford used to make cars affordable for the masses: standardization of activities, specialization of labor and equipment, and a high-volume production line that never stops.

Let’s return to the trio of companies whose value propositions were built around serving a distinct customer. We’ll begin our look at tailored value chains by simply highlighting the major activity choices that reflect each company’s chosen segment, and how those choices are different from those made by rivals who are serving different customers.

The first test of a strategy is whether your value proposition is different from your rivals. If you are trying to serve the same customers and meet the same needs and sell at the same relative price, then by Porter’s definition, you don’t have a strategy

of customers: business travelers, families, and students. Instead of meeting all of the needs of a target customer all of the time, Southwest meets one type of need that many customers have at least some of the time. Southwest created a distinct kind of value that, for many decades, distinguished it from other airlines. Although Southwest has been widely imitated, it would be a mistake to say that Southwest has found the “best” value proposition for the industry. It is only “best” at meeting a particular kind of need at a particular relative price

Even better than the cash was the game-changing insight about Southwest’s customers. Some were clearly more price sensitive, and less time sensitive, than others. Muse acted immediately. He raised the peak fare to $26 and dropped the off-peak fare to $13. Multiple-tier pricing is now standard industry practice, but at the time, it was a major innovation. It allowed Southwest to further segment its customers and to fill its planes. Lower off-peak fares appeal to leisure travelers who are more price sensitive and have greater flexibility about when they travel than do business passengers. Thus Southwest’s value proposition cut across traditional customer segments, appealing, on given occasions, to a variety

And price isn’t the whole story. Southwest was also more convenient. First, its frequent departures allowed customers to travel when they wanted. Second, its flights arrived on time and customers didn’t have to wait in slow lines at the ticket counter. Third, the secondary airports that became central to Southwest’s strategy were closer to downtown, cutting a traveler’s total trip time. These convenience factors were a draw for business travelers. Southwest didn’t figure out every element of its value proposition on Day One. Companies rarely do. It learned by doing. Here’s a classic example of how that happens in practice. In 1971, one of the planes in Houston needed to go to Dallas for routine maintenance over the weekend. Then-CEO Lamar Muse didn’t want to fly the plane empty, figuring that some revenue was better than none. He offered seats on the Friday-night flight for $10, half off the standard $20 fare on that route. The flight sold out, providing some extra cash for the struggling start-up.

Customers are powerful because they are price sensitive and have low switching costs. Rivals, dealing with high fixed costs, compete on price to fill seats. New entrants are a constant threat, because entry barriers are lower than you might think. You can start an airline with a couple of leased planes. Substitutes keep prices down. Customers can choose other forms of transportation, especially on shorter trips. Southwest’s low relative costs provided shelter from the industry’s self-destructive price competition. Moreover, its value proposition gave it a truly unique positioning vis-à-vis that last force, substitution. Its low fares made flying an attractive alternative for price-sensitive travelers accustomed to driving or taking a bus. In the early years, a shareholder asked CEO Herb Kelleher if Southwest couldn’t raise its prices by just a few dollars since its $15 price on the Dallas–San Antonio route was so much lower than Braniff’s $62 fare. Kelleher said no, our real competition is ground transportation, not other airlines. Consider Southwest’s first expansion beyond its original three cities, Dallas, Houston, and San Antonio. It chose Harlingen, Texas, a town in the Rio Grande Valley probably few people have ever heard of. The year before Southwest launched its service, 123,000 passengers used the route the year before Southwest launched service.

Southwest Airlines, the most successful—and the most emulated—airline in the world, has thrived by meeting “just enough” of its customers’ needs at dramatically lower prices. From its humble beginnings flying only to three cities in Texas in 1971, Southwest has grown to be one of the world’s leading airlines, both in size and in profitability. It has done so with a value proposition that for three decades was radically different from other airlines. Southwest didn’t promise to get you anywhere you wanted to go, as other airlines did. Nor did it offer the basic amenities that were once standard industry fare: meals, assigned seats, baggage transfers. Full-service airlines (perhaps a term that no longer accurately describes the legacy carriers, with their higher costs and prices) overserved the needs of a large number of travelers flying Southwest’s shorter point-to-point routes. Southwest’s value proposition put it in a unique position vis-à-vis the five forces. As most know, the airline industry is brutally inhospitable. Suppliers, especially the labor unions but also plane makers, are powerful. Customers are powerful because they are price sensitive and have low switching costs.

Hertz and its followers in the industry built their business around business and vacation travelers. Enterprise recognized that a sizeable minority of rentals, roughly 40 to 45 percent, occur in the renter’s home city. If your car is stolen, for example, or damaged in an accident, you’ll need a rental. In such cases, your insurance company might cover the cost, usually with contractual limits on the price it will pay. About a third of Enterprise’s revenues come from insurers. Other occasions prompt home-city rentals as well—for example, when a car has a mechanical failure or when a child is home from school on vacation. In all of these uses, home-city car renters tend to be more price sensitive than business or vacation travelers. Enterprise crafted a unique value proposition to meet these needs: reasonably priced, convenient, home-city rentals. Compared with Hertz and Avis, Enterprise has chosen to serve a different need at a different relative price. It is not that Enterprise is the best car rental company. Nor is the market it serves inherently better. But starting with the specific need it serves, Enterprise has made a different choice about the value proposition triangle. Enterprise’s customer base would confound traditional market segmentation by demographic characteristics.

Enterprise Rent-A-Car is the market leader in car rental services in North America, where it is bigger than the once-dominant players, Hertz and Avis. Enterprise has also been dramatically more profitable. It is the only major company in the industry that has enjoyed sustained superior profitability, because for decades it pursued a distinctive strategy. The Enterprise value proposition is based on a simple insight: renting a car meets different needs at different times. Hertz and its followers in the industry built their business around business and vacation travelers.